A tariff is a tax imposed by one country’s government on products that are imported from a foreign country. This makes the imported products more expensive as opposed to local alternatives.

Tariffs that are imposed on wine imported from another country will almost certainly increase the end consumer price. Here is an example of a Canadian wine being sold into the U.S. market assuming a 25% tariff (current conditions). The same principles would apply for wines from other countries if the US imposes tariffs as they may do this coming week (although the threatened tariff on European wines is 200% not 25%!).

For example:

With Tariff

Without Tariff

A Canadian winery sells a bottle of wine to a U.S. importer for $10

$10

$10

AT USA BORDER Tariff of 25% imposed by US Govt on Canadian products

+$2.50

+$0

USA BORDER

———————-

———————-

US importer pays tariff to get the wine released from customs. So the $10 cost for the wine increases to $12.50.

$12.50

$10.00

US importer must add $ to cover its expenses and profit (to generate a wholesale price). Assume 20% added. Wine is then sold to a retailer at that price.

$15 wholesale

$12 wholesale

US retailer adds $ to cover its expenses and profit (to generate a retail price). Assume 30% added.

$19.50 retail

$15.60 retail

+$3.90 with tariff

The end consumer will almost certainly pay more for the bottle of wine when tariffs are applied because the US-based importer had to pay the tariff, increasing its costs. In some rare circumstances, the US importer might absorb the increased costs or the Canadian exporter (winery) might lower its prices but this would be unusual.

As a result, tariffs are essentially hidden government taxes that are applied prior to the wholesale level of distribution, thus increasing the cost of goods throughout the supply chain.

Yesterday (March 5th), the federal government issued a first ministers’ statement indicating that significant changes will be made shortly to eliminate or reduce internal trade barriers in Canada: see First Ministers’ Statement on Eliminating Trade Barriers in Canada. Specifically, the announcement states the following regarding barriers that restrict the alcohol trade:

“Launching pan-Canadian direct-to-consumer alcohol sales for Canadian products: The Governments of British Columbia, Alberta, Saskatchewan, Manitoba, Ontario, Quebec, New Brunswick, Nova Scotia, and Canada have committed to improving the trade of alcohol products between participating jurisdictions by advancing direct-to-consumer sales for Canadian products. Currently, British Columbia allows for direct-to-consumer sales for wine, while Manitoba is already open to direct-to-consumer sales on all alcoholic beverages. The Yukon is exploring options for direct-to-consumer alcohol sales within the territory.”

I am encouraged to see that progress may be happening on this issue. However, I have been working on this issue for a decade and a half. During that time, there have been many grand statements of intention with only a few practical and workable results. On this issue, like many areas of liquor policy, the “devil is in the details”. Particularly, I wait to see for those details and to see whether the announced changes address the following two major issues.

Will There Be Realistic and Workable Tax Expectations?

The major stumbling block over the years has been provincial concerns that if they loosen their control over their respective provincial liquor monopolies by removing interprovincial restrictions, they will lose sales tax and liquor markup revenue from liquor sales. The latter amounts are the ‘hidden taxes’ that are applied by the government liquor monopolies at the wholesale level as part of their statutory monopolies over liquor distribution. Generally, the provinces have asserted that they need to collect all of the tax and liquor markup from out of province sales in order to ‘remain whole’. In my view, this concern is exaggerated.

The liquor markup fulfills two functions. Partly, it covers the costs of operating the wholesale liquor distribution system (i.e. importing, warehousing, shipping … and sometimes also retail costs). And partly, it is ‘pure tax’ that goes to general revenue. There are very different approaches to the application of these fees in each province. Sales taxes vary considerably with Alberta having none. There is similar variation for liquor markup with varying amounts charged. Some provinces exempt their own producers from markup entirely (BC) or apply reduced charges (Ontario).

In respect of an interprovincial sale where the wine is shipped directly from a producer to a customer, there are zero liquor distribution system costs to be covered. The destination province incurs no costs at all because the producer or customer pays for the shipping and costs of sale. As such, the provinces should only be worried about the ‘pure tax’ component.

And even on that part, would interprovincial sales make any appreciable difference? Manitoba has had open borders for alcohol sales since 2012 … and has not experienced any meaningful drop in provincial liquor revenue. BC has permitted DTC sales of Canadian wine from other provinces for years (without collecting any fees) … and has not seen any significant adverse effects. Same for Nova Scotia. The reality is that if a province has reasonable tax and markup levels, it will not see any substantial change … because it is much easier for a customer to buy wine locally than to order it from another province, pay for shipping, and wait for delivery. DTC generally only happens in respect of product that is difficult to find and for that small segment of the wine consumer marketplace that is willing to seek out those wines.

For any system that permits the interprovincial sale of alcohol, there needs to be realistic and workable expectations about how much sales tax and liquor markup are being collected, if any. If the system is too expensive or administratively cumbersome, it simply will not work … and may price Canadian wines out of reach of normal consumers.

The recently introduced Alberta DTC system provides an instructive example. When introduced, this system required producers to pay a simply flat fee amount (about $3) on each bottle. This was easy for producers to charge and reasonable enough that consumers would likely pay it. However, Alberta has recently indicated that it is changing its markup structure … and it is not yet clear how much fees will increase or whether the fee calculation will become overly complicated (see Alberta Hikes Liquor Markups).

Consequently, I await the details associated with our new ‘open borders’ for alcohol. It may be too much to hope for truly ‘free’ sales and shipment but I am hopeful that the provinces may at least introduce a sensible system that will work for both producers and customers.

Will Consumers Have Both Producer and Retail Choice?

A secondary concern is whether the new system will apply so that customers can buy wine from both producers and retailers in other provinces. To date, the only province that openly permits both is Manitoba. The reforms in BC and Nova Scotia only apply to Canadian wine purchased directly from a winery. If Canada wants to join the rest of the world, it should let wine lovers shop for wine in other provinces without such limitations … and simply let consumers find, buy and love any wine that they can find within their own country.

What Wine Does the Tariffs Apply To? The Canadian tariffs will apply to all U.S. produced wine that enters Canada as described above. The tariffs would not apply to non-U.S. wine (e.g. French or Italian wine) that enters Canada from the U.S. or from other countries.

When Will the Tariffs Take Effect? The Canadian tariffs take effect as of 12:01 am today (Tuesday March 4th). However, they will not apply to goods that were already in transit to Canada today. As such, these tariffs will apply to all U.S. wine arriving at the border which is shipped today or later. The tariffs are imposed when the product enters Canada so wine that is already within Canada will not be subject to the tariffs. For example, U.S. wine that is already in Canadian stores or is already in the Canadian distribution system will not be subject to the tariffs.

Will Wine Prices Rise Because of the Tariffs? U.S. Wine prices should not rise immediately because wine that is already here will not be subject to the tariffs. Wine importers will likely exhaust their existing stocks of U.S. wine at existing prices so they should be able to supply retailers and restaurants/bars for some time depending upon their stock levels in Canada. Importers will hope that the tariff disputes are resolved before they have to import new stock. If an importer brings in new stock from the U.S., that stock would be subject to the tariffs and the importer would likely have to raise consumer prices (see below).

How Much Could Prices Rise? If an importer brings in new stock from the U.S., there would likely be considerable price hikes. The 25% tariff would be added to the supplier’s cost before the imposition of other taxes and liquor board markups. The cumulative effect creates a multiplier of “tax on tax” which would significantly increase costs for the importer and make it very difficult for them to ‘absorb the cost increase’. For example, using rough calculations, I believe that a U.S. bottle of wine currently retailing for $20 would increase by about $5-6. All price points would be affected with greater dollar price increases at higher price points. I note that the effect in Alberta will be compounded with the recent change in AGLC liquor markup rates.

Will U.S. Wines Still Be Available? What Will be the Effect on Sales? The reciprocal tariffs are an action of Canada’s federal government. However, liquor distribution is controlled by the individual provinces, all of which have government monopolies on distribution at the wholesale level and most of which also have government retail stores. Some provinces have either entirely removed or selectively removed U.S. alcohol products from distribution by their provincial liquor monopolies (update: most Canadian provinces have now entirely removed U.S. alcohol from government monopoly distribution). These actions will obviously have severe marketplace effects. Even in those provinces which continue to permit sales, the effect on consumer purchasing of U.S. wines will likely be significant if this dispute drags on. Some consumers may choose to avoid purchasing U.S. wines due to the politics of the situation. But even for those that don’t, all U.S. wines would become less price competitive as compared to Canadian wines and wines imported from other countries. There would likely be a significant loss of market share from the U.S. in favour of Canada and other countries.

What About Bringing Wine Back After a Trip? The tariffs will not apply for accompanied imports of wine that are within an individual’s duty-free limit. However, they would apply for any amount of wine that is outside the limit. As such, the importation of U.S. wine by a traveller that is not duty-free will become considerably more expensive.

What About Selling Canadian Wine in the U.S.? The American tariffs would affect the price of Canadian wine in the U.S. marketplace in a similar way to that described above (although the U.S. does not import much Canadian wine). As a result, any new shipments of Canadian wine (or other alcohol) into the U.S. would be subject to tariffs with resulting eventual price increases and eventual erosion of market share. This issue would be more significant for Canadian spirits manufacturers.

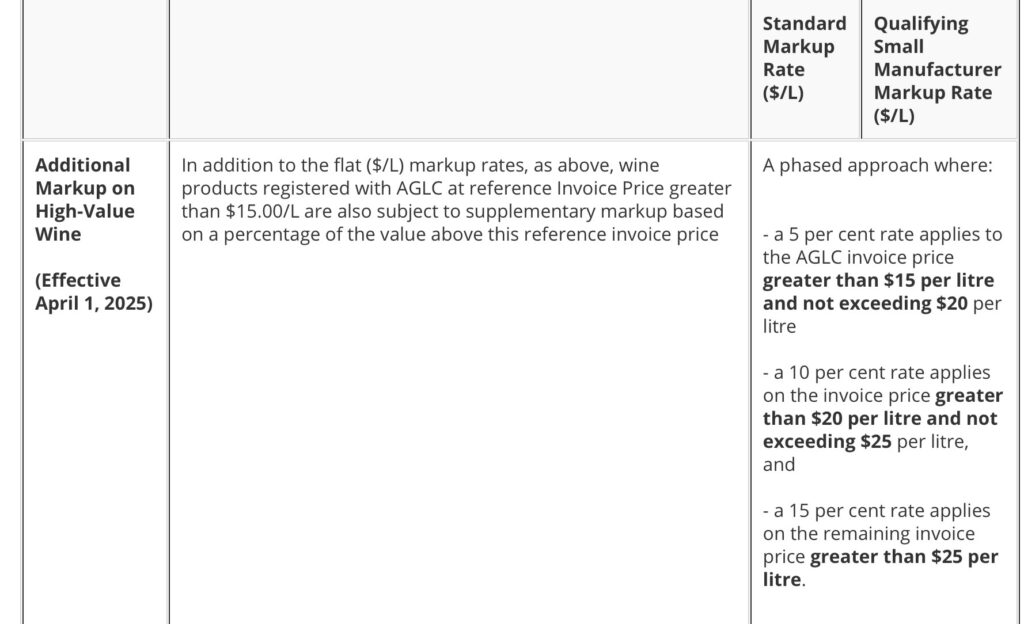

Yesterday, the Alberta Gaming, Liquor and Cannabis Commission (AGLC) announced that liquor markups in Alberta will increase as of April 1st 2025 for “high-value wine”. Liquor markups are government imposed fees applied at the wholesale level as a result of the statutory government monopoly over wholesale liquor distribution. Essentially, they are ‘hidden’ taxes on liquor. Previously, AGLC had applied a volume-based markup on wine, which now increases slightly to $4.11 per litre ($3.08 per 750 ml bottle). This fee remains constant regardless of the value of the wine. This system was often referred to as the ‘flat tax’ and was preferred by many in the industry as being relatively simple. It resulted in prices for wine that were relatively low by Canadian standards.

A new system has now been introduced that is more complicated and imposes additional fees on “high value” wines that are based on the value of the wine (sometimes referred to as ‘ad valorem’ taxes). The flat tax described above still applies for wines that have a “reference invoice price” up to $15 per litre ($11.25 per 750 ml bottle) (I call this “Supplier Cost” below) . Using approximate calculations that would translate to about $20 per 750 ml bottle at retail once the various fees are added in. So wines at or below that consumer price point should be relatively unaffected.

However, for wines above the $15 per litre reference point, there are new additional percentage based fees that are shown in the table below:

AGLC New Wine Markups

As you will note, this system is fairly complicated imposing 3 levels of additional fees, based on the wine’s value. The fees are 5% for value between $15-20 per litre. Then 10% for any value between $20-25 per litre. Then 15% for any value above $25 per litre. Again, using approximate calculations, this would have the following effects. Retail margins vary considerably so the numbers would change accordingly (examples below use a retail ‘markup’ of 38%).

Supplier Cost inc. excise/duty (750 ml)

Flat Tax Markup

Additional ‘High Value’ Markup

Approx Wholesale Price

Approx End-Consumer Price

Approx Price Increase

11.25

3.08

0

14.33

19.78

0

15.00

3.08

0.19

18.27

25.21

0.26

18.75

3.08

0.57

22.40

30.91

0.79

30.00

3.08

2.26

35.34

48.77

3.12

75

3.08

9.01

87.09

120.18

12.43

The new system will create end-consumer price increases as noted and which are more significant as the value of the wine increases. Any value (supplier cost) above $18.75 per bottle will be ‘taxed’ at 15% so the largest increases will occur for expensive wines (above approx. $30 retail). Effectively, Alberta has now introduced a new hidden ‘tax’ of 15% on expensive wine.

The new system becomes effective on April 1st, 2025. I note that it remains unclear how these changes will apply to the recently announced DTC registration system under which BC wineries can sell directly to consumers in Alberta.